- The Street Sheet

- Posts

- Real Estate Sector Snapshot

Real Estate Sector Snapshot

Fundamentals, technical indicators, and trends to watch in the real estate sector

Michele Filippig

August 21, 2024

An introduction to the Real Estate Select Sector SPDR Index (XLRE)

It’s been a tough road for the real estate sector in recent years. As a sector highly sensitive to interest rates, it has been hit hard by the rapid rise in rates.

The Real Estate Select Sector SPDR (XLRE) has historically provided investors with exposure to the real estate sector. It stands out as one of the smaller ETFs within the 11 Select Sector SPDR ETFs, with a market value just below $7 billion—significantly less than the $17.5 billion median across other sectors. As some of the oldest and largest sector ETFs available, they share key features such as low expense ratios of 0.09%, excellent liquidity, and market-cap-weighted structures.

XLRE is moderately concentrated, holding 31 stocks, with its top holding accounting for 11% of the fund (compared to a median of 14% among the other sectors) and its top 10 holdings making up 61% of the fund (vs. a 65% median). Despite its size, XLRE offers an attractive dividend yield of 3.3%, the second-highest across all sectors and more than double the median of 1.6%, trailing only the Energy Sector ETF (XLE).

The chart below highlights XLRE's performance against the S&P 500, starting from March 2022 when the first rate hike took place.

XLRE Performance vs S&P 500 From Start of the Tightening Cycle

Source: Koyfin

A look inside

XLRE is spread out across eight sub-sectors:

Specialized REITs (44%): this category owns properties that don't fit within the other REIT sectors, such as movie theaters or farmland.

Retail REITs (13%)

Residential REITs (13%)

Health Care REITs (12%)

Industrial REITs (10%)

Real Estate Management & Development

Hotel & Resort REITs (1%)

Office REITs (1%).

Top 10 XLI Holdings

Source: SPDR

Some tailwinds

Market wisdom suggests that REITs struggle during periods of rising interest rates and thrive when rates are falling. This sensitivity stems from two main factors: their heavy reliance on debt financing and the direct impact of rate changes on the valuation of their underlying properties, with growth potential playing a relatively minor role.

Currently, the CME consensus, the world’s largest derivatives exchange, anticipates two 25 basis point cuts in September, with a 55% chance of this happening compared to a 45% probability of just one cut. An additional 25 basis point cut is expected by the end of the year, with a 44% probability.

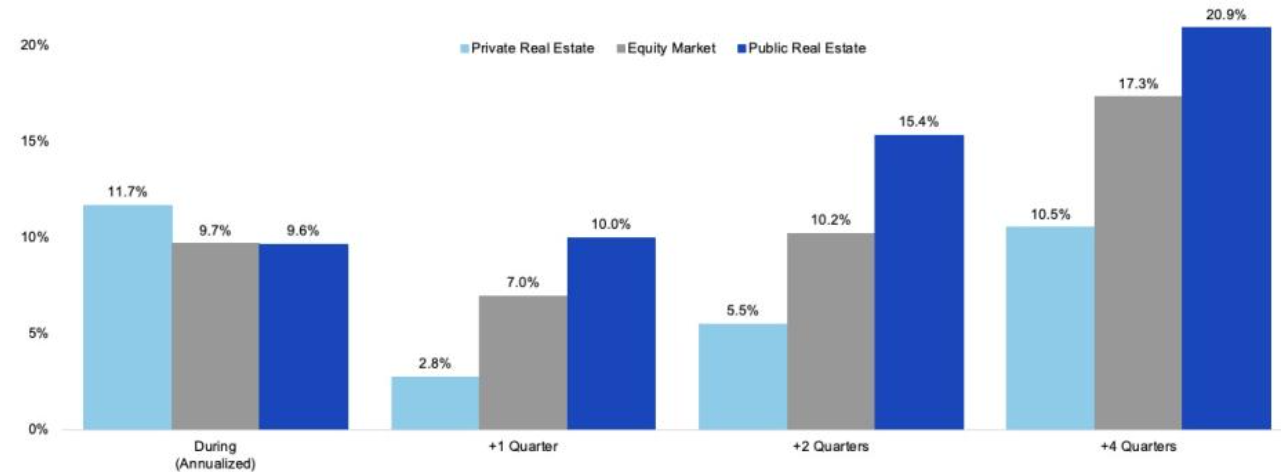

Historically, REITs have performed well after Fed tightening cycles. The chart below illustrates the average performance of private real estate, equities, and public real estate during and after past Fed tightening cycles. The visual encompasses the four full rate hike cycles since 1990: the "soft landing" of 1994-95, the post-dotcom bubble period of 1999-2000, the post-housing boom of 2005-06, and the aftermath of the large rate cuts following the global financial crisis of 2015-18.

Average Total Returns During and After Fed Tightening Cycles

Source: Nareit

Key risks

The recent July jobs report revealed a rise in the unemployment rate to 4.25%, sparking increased concerns about a potential hard landing for the economy. This fear is mirrored in the 10-year Treasury rates, which have dropped significantly since the report's release, falling below 4% for the first time in nearly two years. This ongoing volatility in interest rates introduces considerable uncertainty for XLRE, with the potential for both upside and downside movement.

Reply