An overview

For the week ending on August 9, over 90% of S&P 500 companies had reported their Q2 results. The data reported was overall promising. A solid 59% of the companies have delivered positive revenue surprises, while 78% have exceeded EPS expectations.

While the percentage of companies surpassing earnings forecasts slightly outpaces the historical average (77% over the past five years), the magnitude of these surprises is more modest. On average, companies are reporting earnings 3.5% above estimates, below the 5-year average of 8.6%.

The sectors driving these positive earnings surprises include Utilities (+9.3%), Health Care (+8.5%), Consumer Discretionary (+7.7%), and Financials (+7.6%). Communication Services was the only underperformer reporting an aggregated -12% negative EPS surprise, bucking the overall trend.

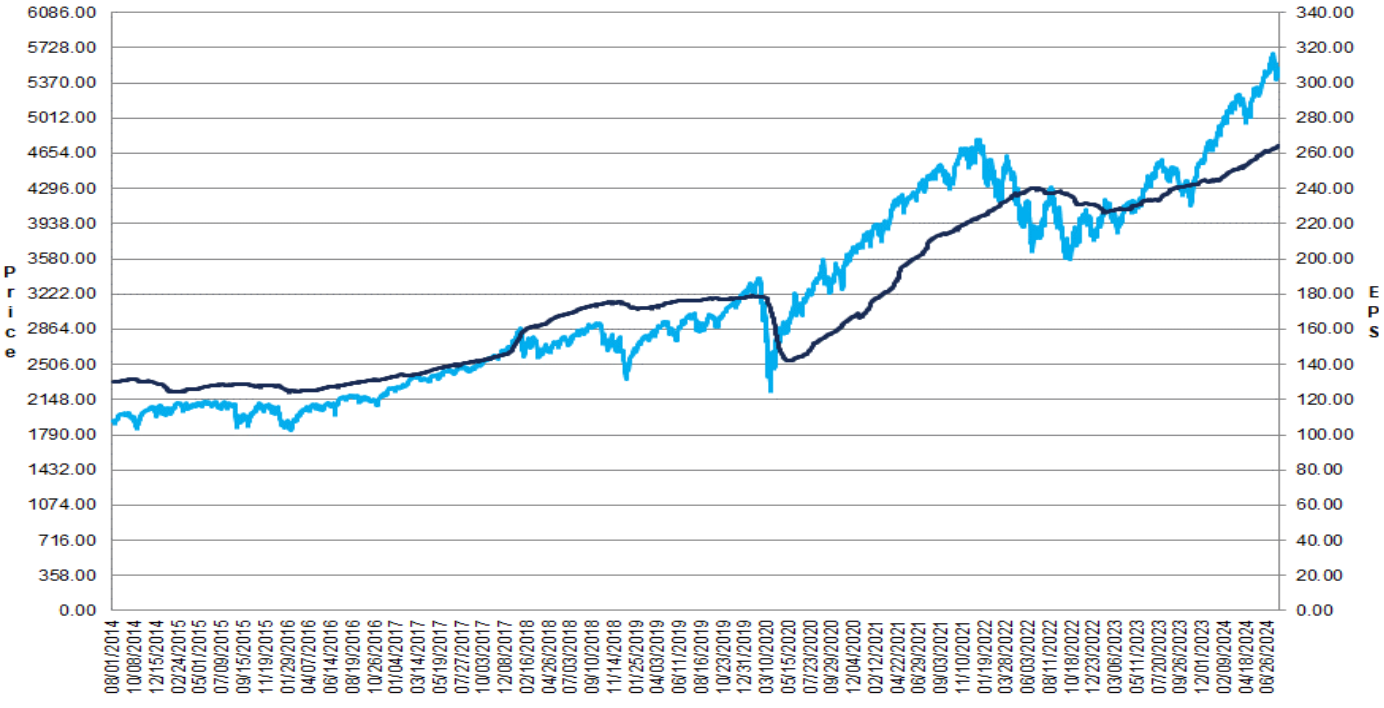

S&P 500 Price vs Forward 1-year EPS ($) Over the last 10 years

Source: FactSet

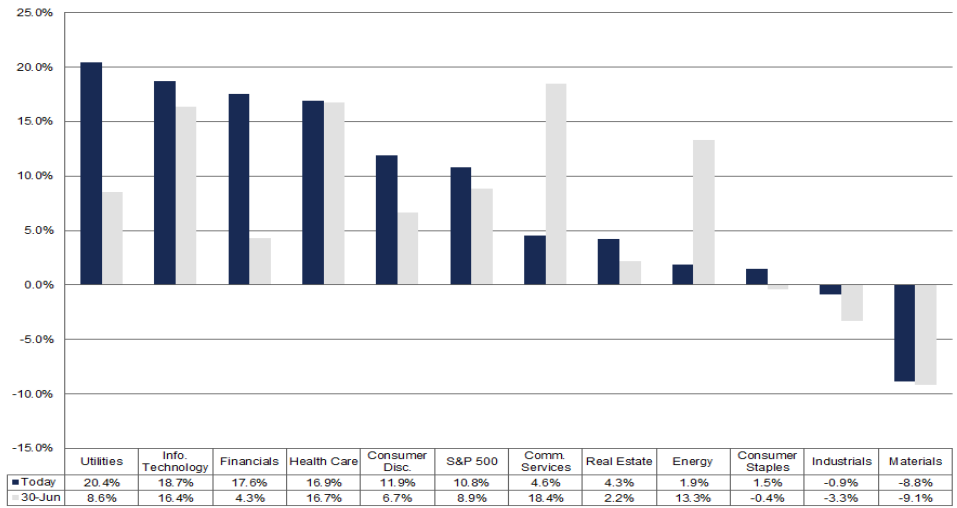

Strongest YoY earnings growth since post-pandemic rebound

In 2Q24, the blended YoY1 growth rate stands at an impressive 10.8%. If this figure holds, it will mark the strongest earnings growth since 4Q21’s 31% hike and the index's fourth straight quarter of growth. Notably, nine out of 11 sectors are posting YoY growth, with five of them — Utilities, Information Technology, Financials, Health Care, and Consumer Discretionary — showing double-digit gains.

On the other hand, two sectors are experiencing a decline in earnings, with Materials leading the drop. Looking ahead, analysts forecast YoY earnings growth of 5.4% in 3Q24 and a robust 15.7% in 4Q24 (10.2% growth for the full year).

S&P 500 2Q24 Earnings Growth YoY by Sector - Actual vs Consensus Estimates

Source: FactSet

The market is punishing negative EPS surprises more than usual

Companies delivering positive earnings surprises for Q2 2024 have enjoyed an average stock price bump of +0.8% in the two days before and after their earnings announcements. This performance is below the 5-year average gain of +1.0% for similar surprises. Conversely, companies with negative earnings surprises have faced an average price drop of -3.8%, a bit steeper than the 5-year average decline of -2.3% during the same timeframe.

Are Wall Street analysts worried about an economic slowdown?

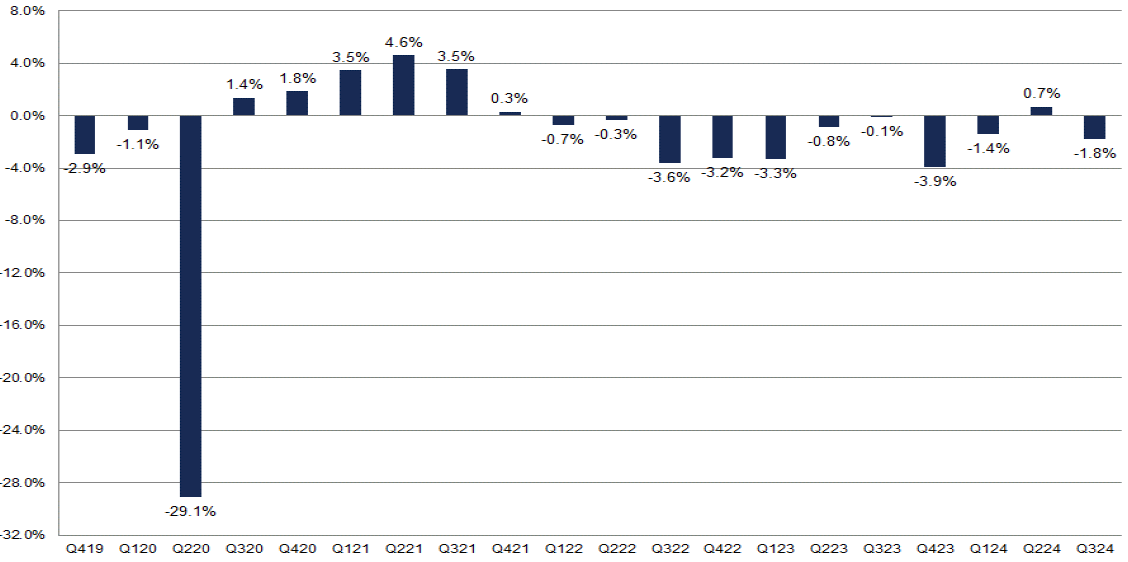

Overall, Wall Street analysts are not concerned about an economic slowdown. In July, the Q3 EPS estimate — reflecting the median earnings predictions for all companies in the index — dropped by 1.8%, which is in line with the average reduction over the past decade (40 quarters). This suggests that analysts typically trim earnings forecasts during the first month of a quarter.

At the sector level, 10 out of 11 sectors saw their Q3 2024 bottom-up EPS estimates decline between June 30 and July 31, with Energy (-6.6%), Industrials (-5.1%), and Health Care (-4.0%) leading the reductions. Interestingly, Utilities (+0.1%) was the only sector to see a slight increase in its EPS estimate for the quarter. While analysts cut Q3 2024 EPS estimates by 1.8% in July, they made virtually no changes to their full-year 2024 EPS estimates, trimming them by less than 0.1%.

Change in S&P 500 Quarterly EPS Estimate During the 1st Month of the Same Quarter

Source: FactSet

[1] Combines actual results for companies that have reported and estimated results for companies that have yet to report.