Happy Sunday to everyone on The Street.

You asked, we answered.

We ran a special “Equity Research” edition of our newsletter ahead of the election, and asked you, our readers, whether you’d like more in the future. The response was a resounding, “Yes.”

So, for the next two weeks, we’ll interrupt your usual Sunday programming with a deep dive into a stock that may be impacted by the upcoming holidays.

Hope you had a great Thanksgiving, a fruitful Black Friday, and a relaxing weekend so far. With Cyber Monday around the corner, you just might need it.

Happy shopping!

Before we dive in, here’s a quick word from our sponsor:

Sponsored By Frec

What if you could passively invest in the market while potentially saving thousands on your taxes?

It’s called Direct Indexing. And it takes zero additional effort.

Let's take the ETF SPY, for example. Which tracks the S&P 500...

Now imagine instead of owning the ETF, you owned all of the individual stocks of SPY...

When an individual stock loses value, you can harvest its loss by temporarily swapping it for a different one while still tracking the index...

These losses accumulate over time and can then be used as a deduction against your tax bill. This is what we mentioned before about tax loss harvesting, which can potentially save you thousands of dollars.

Best of all, it's all completely automated with Frec so you don't have to lift a finger.

Click here to learn more and start investing with Frec today.

St. Sheet is not a Frec customer and Frec paid a one-time fee for this full sponsorship. Investing involves risk, including the risk of loss. Brokerage services provided by Frec Securities LLC, member FINRA/SIPC and advisory services provided by Frec Advisers LLC, an SEC RIA. Both wholly owned subsidiaries of Frec Markets, Inc.

Off Target

When you think of retail stocks poised to benefit from the holiday shopping season, there’s a good chance Target Corporation (TGT) is among the first to come to mind.

Or, at least, it was.

Target turned in its latest quarterly earnings the other day, and its stock subsequently slumped more than 20%. Specifically, its holiday shopping forecast spooked investors. Target projected lackluster sales, despite a rosy outlook for the broader economy.

The retail giant clawed back some of those losses last week, but remains down more than 11% over the past month. But is this a rational reaction to the report, or has the pendulum swung too far?

Let’s dive in.

Executive Summary

The consensus recommendation for Target among analysts is a Buy. The average target price on the stock stands at $143, implying more than 8% upside potential in the near term from current levels.

The stock is currently trading near its 52-week low of around $120. The earnings miss and subsequent stock drop may be an attractive entry point for long-term investors, given the company's significantly discounted valuation relative to peers.

Company & Industry Overview

Target, founded in 1962, is a leading player in the US retail industry. It operates a network of approximately 2,000 stores, as well as a growing e-commerce platform.

The company's business model is centered on offering a broad range of products, including groceries, apparel, home goods, and electronics, while focusing on value and convenience for customers.

Its private-label brands in particular have recently proved pivotal in driving customer loyalty and enhancing profit margins.

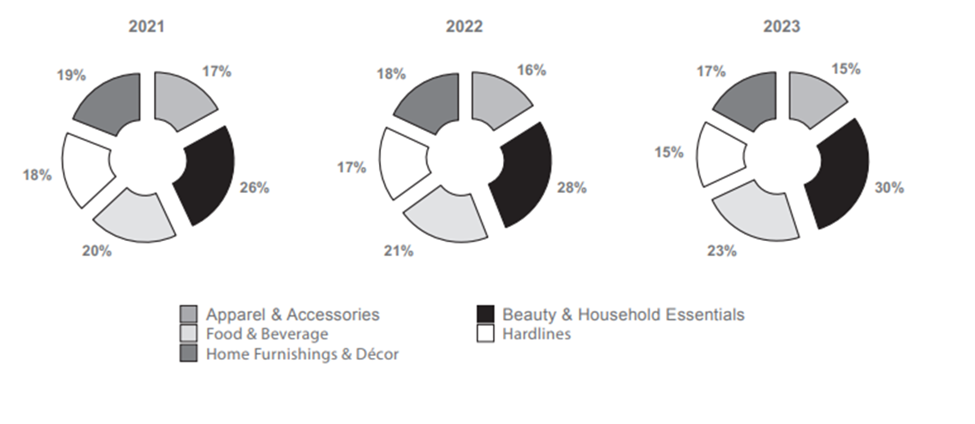

Sales by Merchandise Category

Source: Target's Annual Report 2023

The retail industry itself is undergoing transformative shifts, with e-commerce continuing to gain traction. According to industry reports, online retail is expected to grow at a CAGR of 10% through 2027, with much of this growth driven by categories such as groceries and home essentials — areas where Target has increased its focus.

The Bull Case

The bull case for Target is pretty straightforward: it’s a well-established retailer with a strong foothold in the US market.

A key driver for Target's growth is its omnichannel model, which integrates physical and digital shopping experiences. By offering services such as same-day delivery, curbside pickup, and partnerships with platforms like Shipt, Target has positioned itself as a leader in the hybrid retail space.

These initiatives have helped drive customer loyalty and bolster online sales, which have consistently grown and contributed to the company's top-line revenue. In 2023, online sales accounted for approximately 18% of the company's total revenue, reflecting its strong digital presence.

Target's private-label brands in particular continue to perform well and offer higher margins when compared to national brands. These brands resonate with cost-conscious consumers, a key demographic in the current economic environment.

The Bear Case

Despite these strengths, Target still faces headwinds. Shrinking profit margins, driven by elevated labor and logistics costs, remain a concern.

Additionally, the mega-retailer is unusually exposed to discretionary categories, such as apparel and home goods. These categories continue to underperform amid tighter consumer budgets and a cautious spending environment.

Perhaps most notably, the retailer has been losing ground to its competitors. Target contends with fierce competition from Walmart, which benefits from superior pricing power, and Amazon, which dominates the online space — and its market share is suffering for it.

Financial Analysis & Valuation

Target’s financial performance has faced challenges in recent quarters due to declining consumer spending in discretionary categories and inflationary pressures.

Target's Q3 2024 earnings showed EPS of $1.85 for the quarter, well below the consensus estimate of $2.30. It also lowered its full-year guidance to a range of $8.30–$8.90 per share. Comparable sales growth for the quarter was flat at +0.3%, missing management's prior guidance of flat to +2%. Target's gross margin fell 20 basis points year-over-year to 27.7%, while its operating margin declined 60 basis points to 4.6%.

However, management expects these pressures to ease in Q4 as inventory levels normalize and cost-reduction initiatives take effect. Looking ahead to FY2025, Target anticipates modest growth, supported by improved inventory management and operational efficiencies.

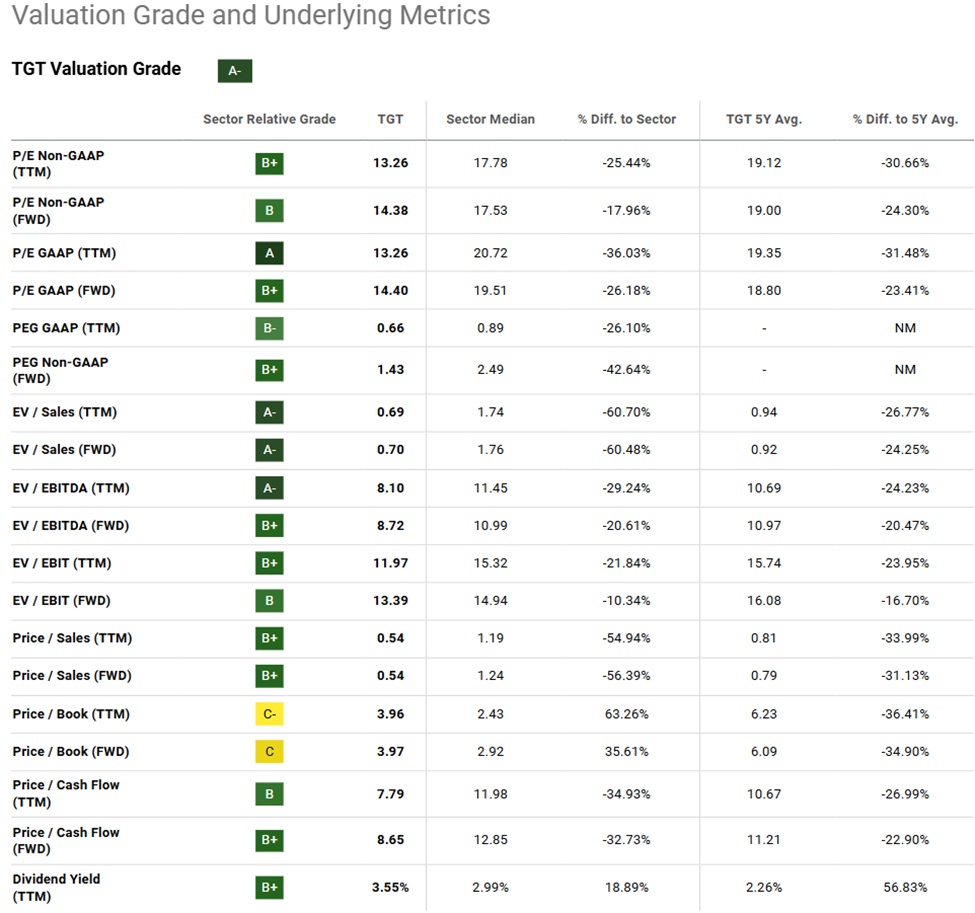

From a valuation perspective, Target remains attractive. Trading at a forward P/E of 13.2x, the stock trades significantly below its 5-year average of 19x. Target's forward EV/EBITDA ratio of 8.7x also suggests potential upside, particularly as operational improvements materialize.

Valuation Grade & Underlying Metrics

Source: SeekingAlpha

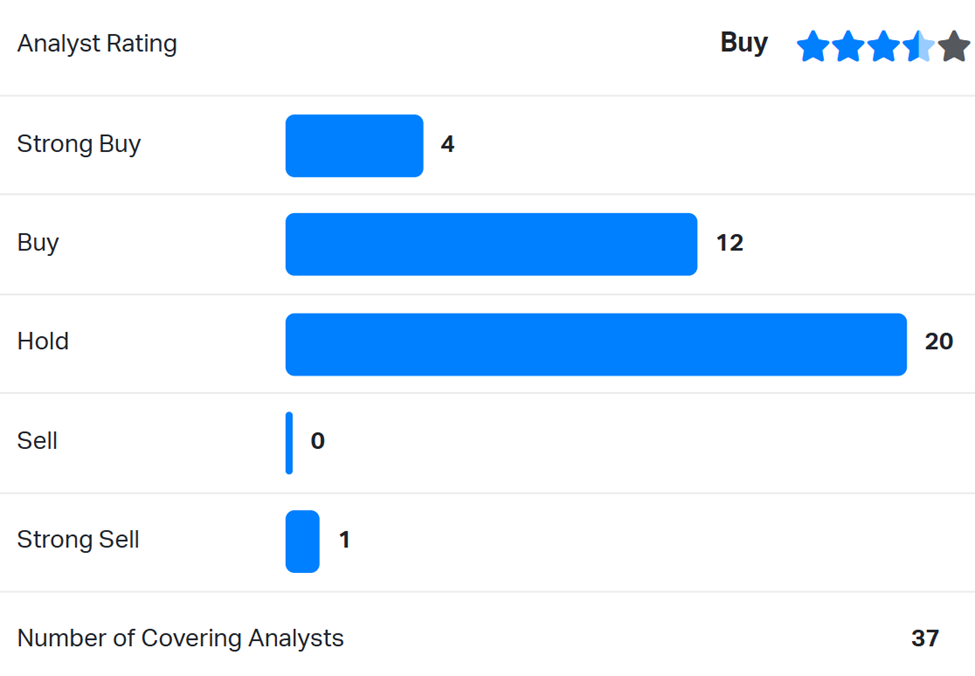

The analyst consensus on Target reflects a generally positive outlook, with an average Buy rating from a broad group of analysts. Target's current stock price of $132 positions it well below the average price target of $143.

Analyst Ratings on Target Corporation

Source: Koyfin

Target's Q3 2024 earnings miss and subsequent guidance cut were disappointing, but the market's reaction may be overdone.

The stock currently trades well below its 5-year average, which could present an opportunity for long-term investors. Target's strategic focus on digital transformation, private-label brands, and operational efficiency provides a strong foundation for recovery, even as macroeconomic challenges and headwinds persist.

Sponsored By Frec

What if you could passively invest in the market while potentially saving thousands on your taxes?

It’s called Direct Indexing. And it takes zero additional effort.

Let's take the ETF SPY, for example. Which tracks the S&P 500...

Now imagine instead of owning the ETF, you owned all of the individual stocks of SPY...

When an individual stock loses value, you can harvest its loss by temporarily swapping it for a different one while still tracking the index...

These losses accumulate over time and can then be used as a deduction against your tax bill. This is what we mentioned before about tax loss harvesting, which can potentially save you thousands of dollars.

Best of all, it's all completely automated with Frec so you don't have to lift a finger.

Click here to learn more and start investing with Frec today.

St. Sheet is not a Frec customer and Frec paid a one-time fee for this full sponsorship. Investing involves risk, including the risk of loss. Brokerage services provided by Frec Securities LLC, member FINRA/SIPC and advisory services provided by Frec Advisers LLC, an SEC RIA. Both wholly owned subsidiaries of Frec Markets, Inc.

Are you bullish or bearish on the oil industry under Trump?

🟩🟩🟩🟩🟩🟩 🐂 Bullish

🟨🟨🟨🟨⬜️⬜️ 🐻 Bearish

Are you bullish or bearish on Roku (ROKU) over the next 12 months?

🟩🟩🟩🟩🟩🟩 🐂 Bullish

🟨🟨🟨🟨⬜️⬜️ 🐻 Bearish

Which stock do you think will outperform over the next 12 months?

🟨🟨🟨🟨🟨⬜️ Arista Networks (ANET)

🟩🟩🟩🟩🟩🟩 Vertiv Holdings (VRT)