- The Street Sheet

- Posts

- Materials Sector Snapshot

Materials Sector Snapshot

Fundamentals, technical indicators, and trends to watch in the materials sector

Michele Filippig

September 05, 2024

An introduction to the Materials Select Sector SPDR Index (XLB)

The materials sector has recently underperformed, trailing the S&P 500 by over 10% in the last twelve months as evidenced by the Materials Select Sector SPDR (XLB).

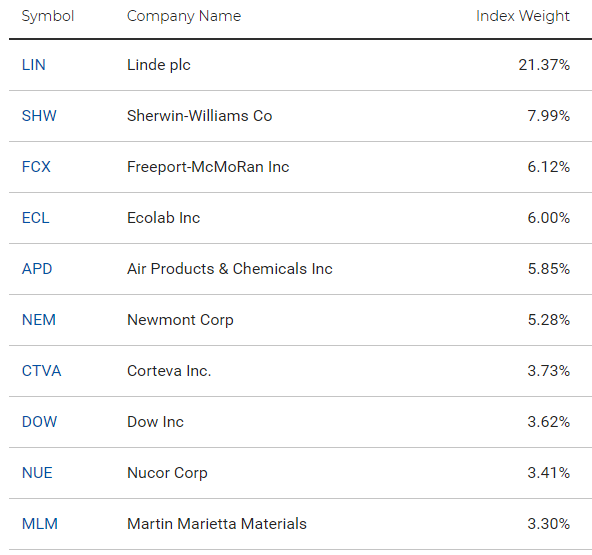

The Materials Select Sector SPDR stands out as one of the smallest ETFs within 11 Select Sector SPDR ETFs with a market value just above $5.5 billion—significantly below the $17.5 billion median across other sectors. XLB is quite concentrated, holding just 28 stocks, with its top holding accounting for 21% of the fund (compared to a median of 14% among the other sectors).

Additionally, its top 10 holdings comprise 67% of the fund (vs. a 65% median). The ETF offers a dividend yield of 1.8%, slightly above the median from all sectors.

A look inside

XLB is spread out across four sub-sectors:

Top 10 XLB Holdings

Source: SPDR

The economic environment in which the basic materials sector typically performs the best is during a period of strong global real GDP growth and elevated inflation. Real GDP growth leads to widespread investment, increasing industrial capacity through investments requiring large amounts of basic materials, like new factories.

On the other hand, if demand for goods and services declines, the high fixed costs of materials companies hurt profitability. Elevated inflation allows these firms to raise prices, and they can pass on more cost increases than other sectors since they sit at the start of the value chain.

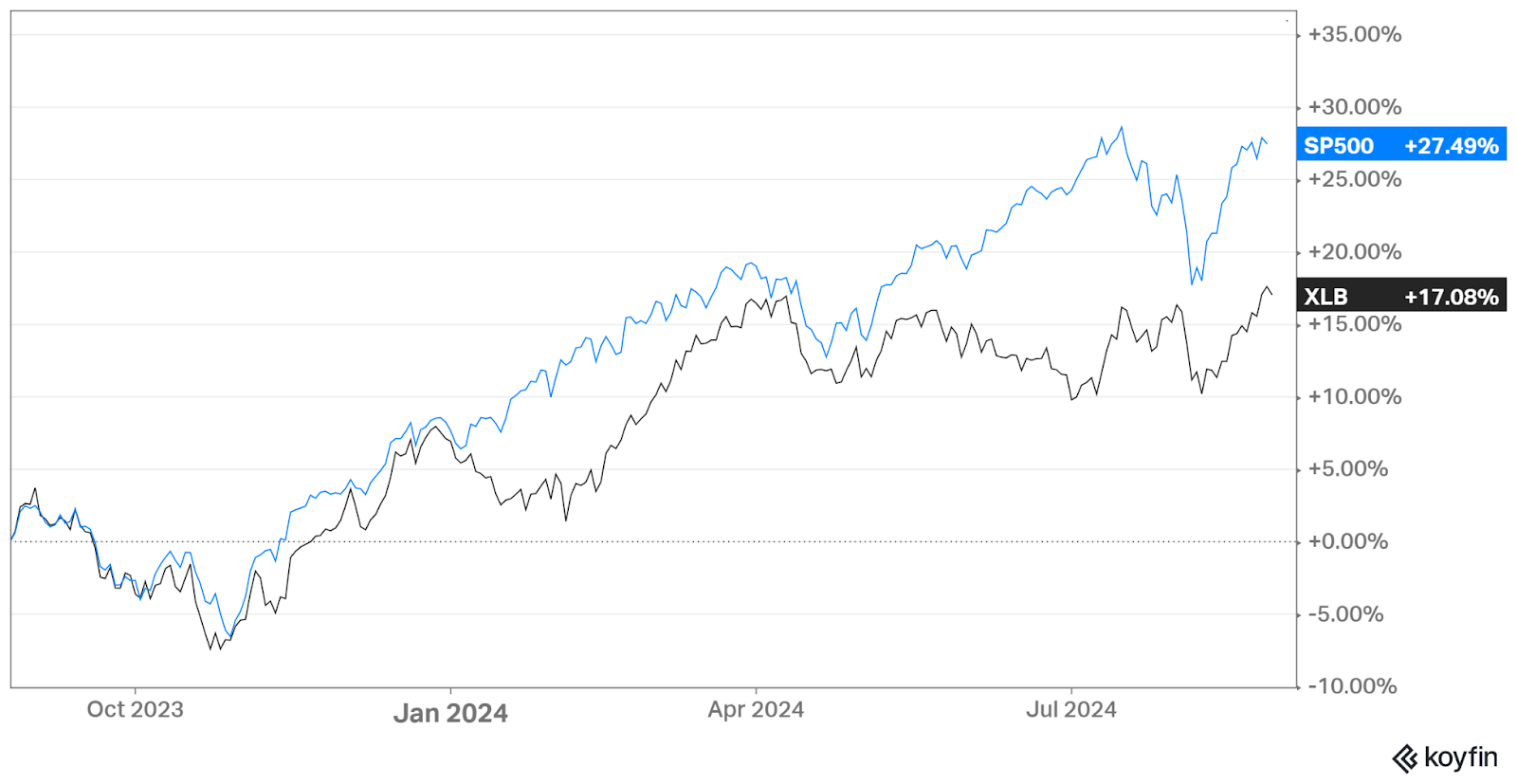

XLB Performance Versus S&P 500 - Last Twelve Months

Source: Koyfin

Underperforming the market

The XLB fund has underperformed in the past 12 months, lagging behind the S&P 500 by more than 10%. This underperformance, which worsened from 2Q24 onward, is largely due to a decline in overall commodities prices, as evidenced by the CRB Commodity Index, since materials companies tend to move in sync with commodities prices. The decline in commodities prices was largely driven by China's slowing economy.

A strong US Dollar has also been a headwind, as commodities are commonly priced in dollars, impacting global demand and further affecting the sector.

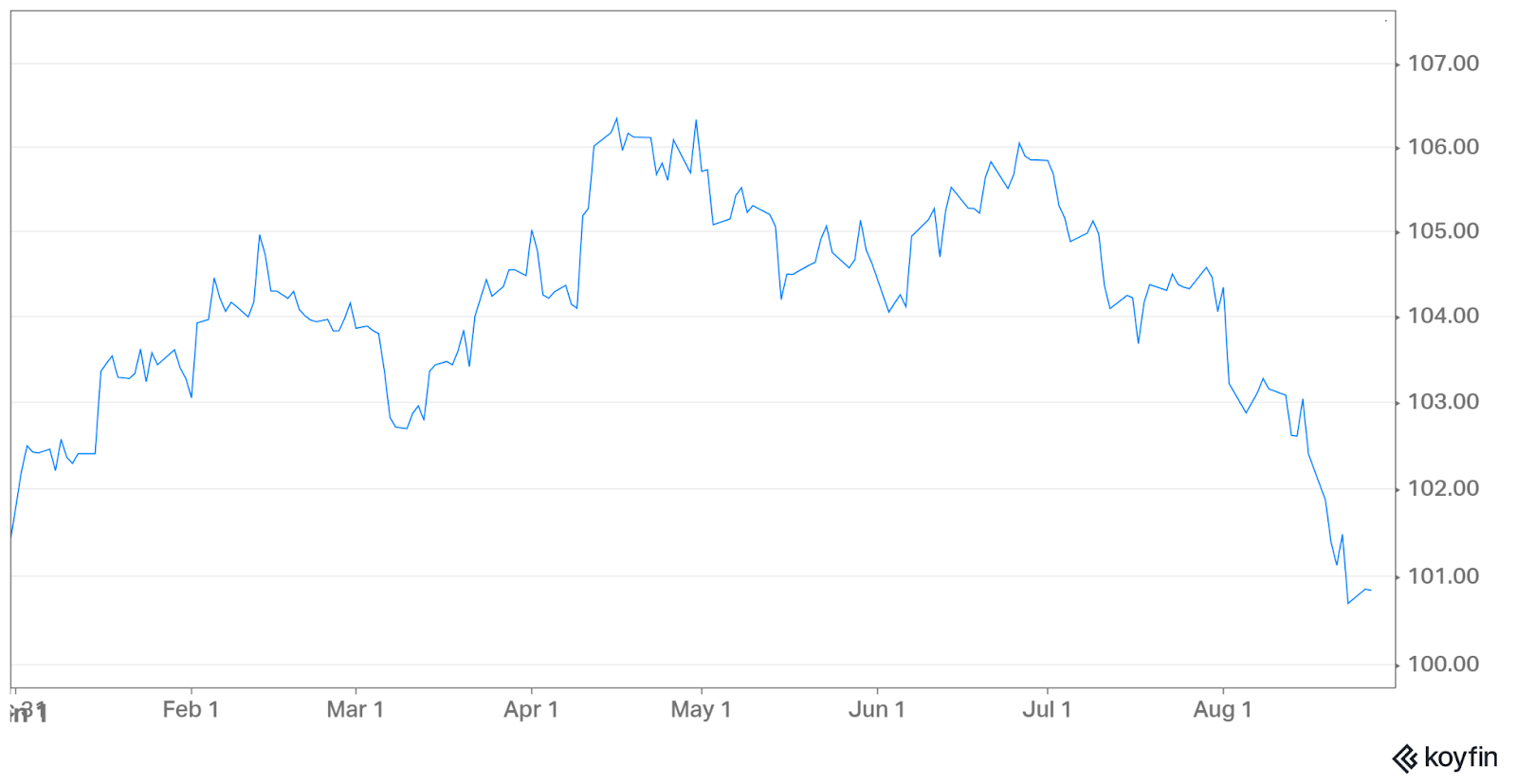

There could be a change on the horizon, as the CRB Commodity Index appears to have bottomed out in early August, and the US dollar is weakening from its June highs, driven by market expectations of Fed rate cuts in September.

CRB Commodity Index

Source: Trading Economics

United States Dollar Index (DXY)

Source: Koyfin

Reply