- The Street Sheet

- Posts

- Healthcare Sector Snapshot

Healthcare Sector Snapshot

An analytic view of fundamentals and trends within the healthcare sector

Michele Filippig

August 07, 2024

An introduction to the Health Care Select Sector SPDR Index (XLV)

The healthcare sector is a defensive growth sector characterized by low correlation with global macro conditions. Investors looking to gain exposure to the sector often consider XLV, an ETF tracking a subset of the S&P 500 called the Health Care Select Sector Index. Launched in 1998, it’s one of the oldest and largest healthcare ETFs. With a low expense ratio of 0.09%, XLV offers an affordable way to invest in the sector, providing a market-average dividend yield of 1.5%.

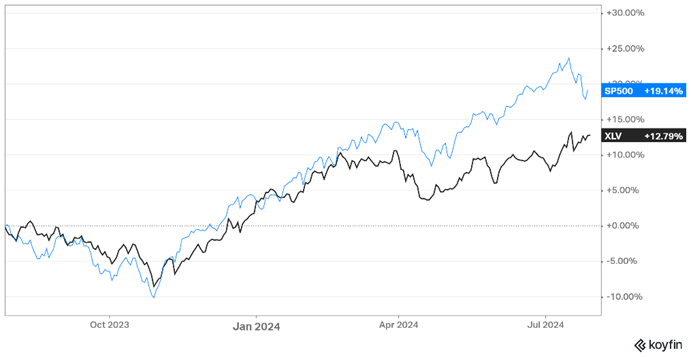

12-Month XLV Performance Versus S&P 500

Source: Koyfin

A look inside

XLV is market-cap weighted with 63 holdings spread out across five primary sub-sectors:

Pharmaceuticals (31%): Research, development, and commercialization of drugs, vaccines, and biotech products.

Health Care Providers (22%): Healthcare facilities, managed care organizations, and ancillary service providers.

Health Care Equipment and Supplies (19%): Manufacturers and distributors of medical devices, diagnostic equipment, and supplies.

Biotech (17%): Companies developing innovative therapies and diagnostic tools using biological processes.

Life Sciences Tools and Services (11%): Suppliers of instruments, consumables, and services for research, development, and production in life sciences.

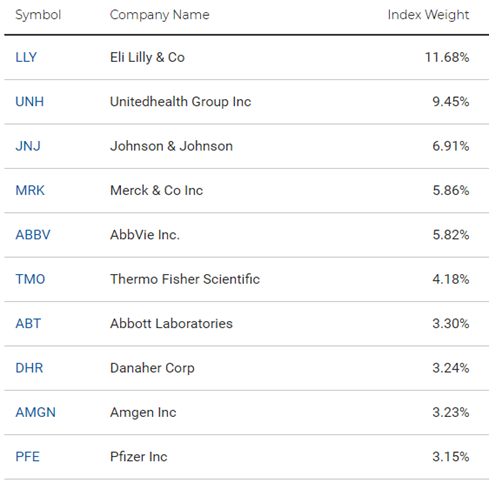

XLV's market cap exceeds $40 billion, with the top 10 holdings comprising over 55% of the index.

Top 10 XLV Holdings

Source: SPDR

Some tailwinds

The demand for health care is generally inelastic and defensive, and XLV currently has a 1-year beta of 0.8 (versus the S&P 500). The sector tends to hold up during economic downturns, like the one we could be nearing. More importantly, The US population is aging rapidly. The 65-plus age group is projected to rise from 58 million in 2022 to over 80 million by 2050, increasing its share of the total population from 17% to 23%. For perspective, in 2000, there were 35 million individuals aged 65-plus in the US, comprising 12% of the population. This growing need for medical treatment and health care services will drive demand for new treatments, medical devices, and efficiencies in the health care system. Moreover, the health insurance system ensures regular and non-optional payments, cementing the inelasticity of demand. The percentage of uninsured Americans has dropped significantly over the last decade, from 15% in 2012 to 8% in 2022. If an economic slowdown persists and there is a rotation out of tech, health care should benefit greatly.

Key risks

The healthcare industry faces significant regulation and scrutiny. Patent expirations and pricing pressures can greatly diminish growth potential. The two biggest challenges in the coming years could include the Inflation Reduction Act and a patent cliff. The Inflation Reduction Act of 2022 aims to reduce Medicare spending on prescription drugs, which could reduce profits for many top holdings in XLV, particularly drug manufacturers. There’s also the looming issue of a patent cliff. Many major patents are set to expire between now and 2030, potentially causing a loss of up to $180 billion in sales across the largest pharma firms, according to Alta Vista Research.

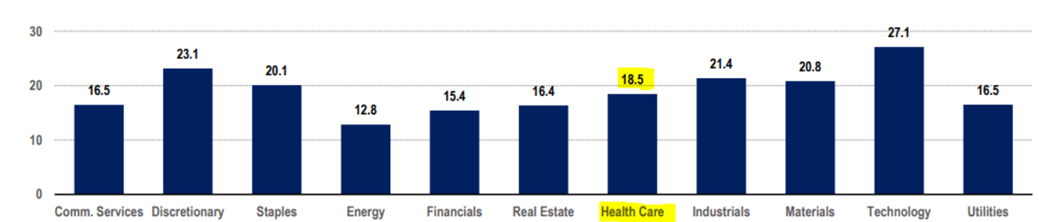

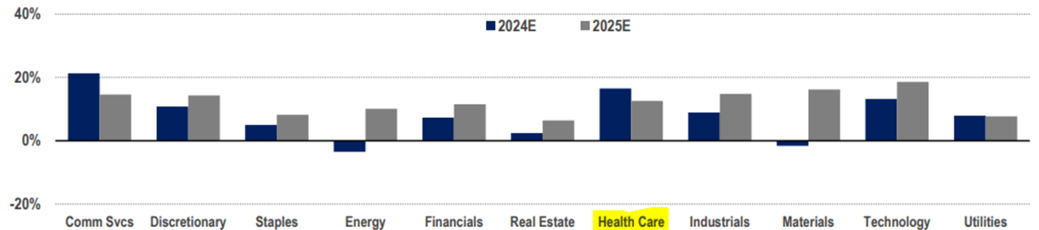

Regarding valuation, the sector's higher profitability and stable cash flows usually result in high valuation multiples. Critics argue that some large drug companies in this ETF may be overpriced. For instance, Eli Lilly (LLY) is currently trading at a forward 12-month P/E of 55x and an EV/EBITDA of 42x, already pricing in significant upsides from weight loss drugs. However, the healthcare sector carries a lower average price-to-earnings ratio than the S&P 500, with XLV trading at a forward 12-month P/E at 21x vs the S&P 500 at 23x. Despite this, healthcare has one of the highest earnings-per-share growth among all sectors.

S&P 500: Price-To-Earnings Ratio (On 2024 EPS) Across Sectors

Source: AltaVista Research

S&P 500: Earnings per Share Growth Across Sectors

Source: AltaVista Research

Reply