Over the past 12 months, the financial services sector has outperformed the broader market, as evidenced by the Financials Select Sector SPDR (XLF). As one of the 11 Select Sector SPDR ETFs, the fund tracks the performance of the sector.

The Select Sector SPDR ETFs encompass all the constituents of the S&P 500. As some of the oldest and largest sector ETFs available, they share key features such as low expense ratios of 0.09%, excellent liquidity, and market-cap-weighted structures.

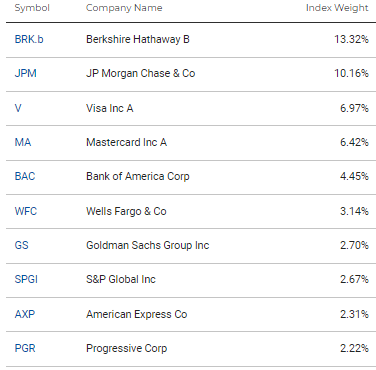

Honing in on the Financials Select Sector SPDR ETF, it stands out as one of the largest ETFs, with a market value just above $40 billion—significantly above the $17.5 billion median across other sectors.

XLF is also one of the most diversified Sector ETFs, holding 71 stocks, with its top holding accounting for 13% of the fund (compared to a median of 14% among the other sectors). The ETF's top 10 holdings make up 54% of the fund (vs. a 65% median). XLF offers a dividend yield of 1.6%, aligned with the median from all sectors.

A look inside

XLF is spread out across five sub-sectors:

Top 10 XLF Holdings

Source: SPDR

Outperforming the market

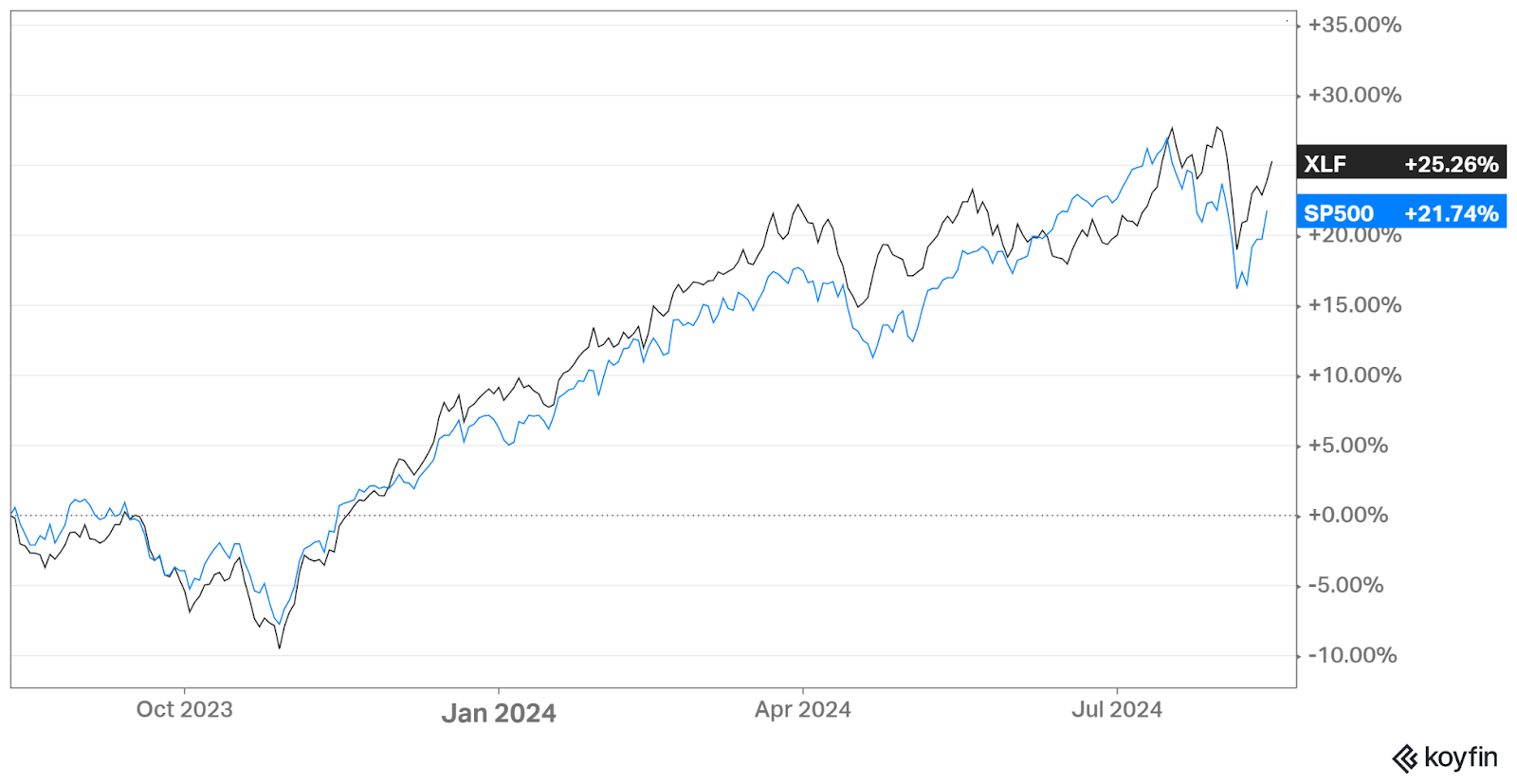

The XLF fund has outperformed the S&P 500 by 3.5% over the last twelve months. This performance has largely been driven by robust consumer spending, increased credit card usage, and higher interest rates. These higher interest rates have helped banks as they benefit from a net interest margin, the difference between the interest rate the banks earn from investing and the interest rates they pay out to customers.

XLF Performance Versus S&P 500

Source: Koyfin

Key risks

However, these driving factors are expected to weaken in the near future, and there are a few data-driven trends that can offer insight. Although increased credit card transactions and balances boost bank profits, the surge in delinquencies poses a significant concern. US delinquency rates on credit card loans—representing overdue debt—have reached alarming levels. In April of this year, delinquency rates exceeded 3%, marking the highest level since 2012.

Delinquency Rate on Credit Card Loans, All US Commercial Banks

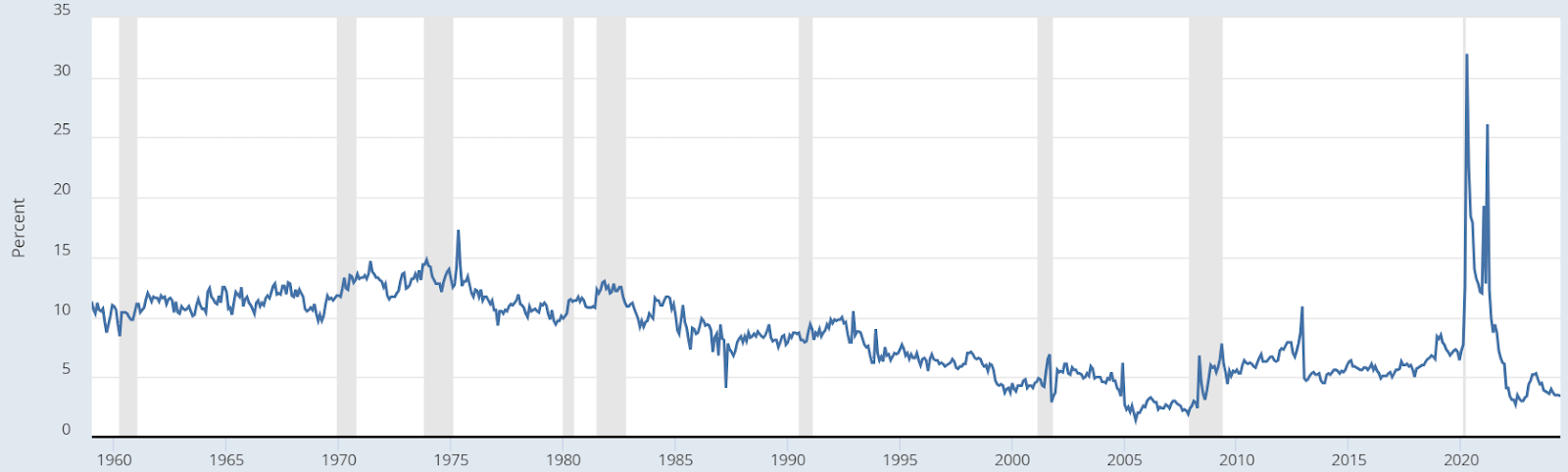

The US personal savings rate is another risk factor for the financial sector. Higher savings rates typically lead to greater inflows for banks, enhancing their investment capacity. Unfortunately, the current US personal savings rate—just 3.4% of disposable personal income—is one of the lowest recorded since 1960.

While a recession has been avoided so far, this low savings rate leaves Americans with little financial cushion in the event of an economic downturn. Without sufficient savings, those who face unemployment are more likely to default on loans, increasing the risk of delinquencies for banks.

US Personal Savings Rate

Some tailwinds

Despite the anticipated challenges, the top holdings in XLF have taken robust defensive measures to navigate these risks.

Berkshire Hathaway (BRK), XLF’s largest holding, has maintained a substantial cash position to weather potential financial storms. Earlier this year, Warren Buffett expressed confidence in Berkshire's ability to withstand financial disasters of unprecedented scale. In Q1, Berkshire's total cash and short-term investments surged to nearly $189 billion—a 44% increase from Q1 2023.

Meanwhile, JPMorgan (JPM), the fund’s second-largest holding, has bolstered its defenses by setting aside a $3.05 billion provision for credit losses, surpassing the estimated $2.78 billion in expected losses.

The Street Sheet (SS) and its principals are not affiliated with any of the assets mentioned above or in this article. The Street Sheet and its principals do not own any of the stocks mentioned in this email and/or web post. The Street Sheet is a research service not owned or managed by registered brokers and therefore this site does not make any investment recommendations. The information provided in this newsletter is not guaranteed as to the accuracy or completeness. Each user of SS chooses to do trades at their sole discretion and risk. SS is not responsible for gains/losses that may result in the trading of these securities. This newsletter includes paid advertisements. The source of all third-party content in which SS receives some sort of compensation is clearly and prominently identified herein as "ad", "Sponsored", or “Together With”. Although we have sent you these advertisements, SS does not specifically endorse any third-party product nor is it responsible for the content, the accuracy, or the completeness of the advertisement or the experience with the third-party advertiser. Furthermore, we make no guarantee or warranty about what is in the advertisement. All investments involve risk, losses may exceed the principal invested, and the past performance of a security, industry, sector, market, or financial product does not guarantee future results or returns. This communication from The Street Sheet is for informational purposes only. It is not intended to serve as a recommendation to buy, sell, or hold any security and is not an offer or sale of a security. Information contained within should not be perceived as a research report and is not intended to serve as the basis for any investment decision. Any third-party views reflected herein do not reflect the opinion of The Street Sheet. All investments involve risk and the past performance of a security does not guarantee future results or returns. There is always the potential for financial loss when investing in securities or other financial products. The information contained in this newsletter is subject to change without notice, and we do not undertake any obligation to update it. Readers are encouraged to conduct their own research and due diligence and seek advice from licensed professionals regarding their specific financial needs and circumstances. By reading this newsletter, you agree to hold us harmless from any and all losses, liabilities, costs, or expenses arising from your use or reliance on the information provided. There is no warranty as to the accuracy or completeness of the factual matters included in any advertisement or sponsored content in the newsletter. You have not performed any research on any entity, or its business, that advertises or submits any sponsored content. The Street Sheet is reader-supported. When you buy through links on our site, we may earn an commission.