- The Street Sheet

- Posts

- AI on Fire, Oil in the Mire: The Q3 Earnings Rollercoaster

AI on Fire, Oil in the Mire: The Q3 Earnings Rollercoaster

Q3 earnings expectations for key sectors and companies

Michele Filippig

September 19, 2024

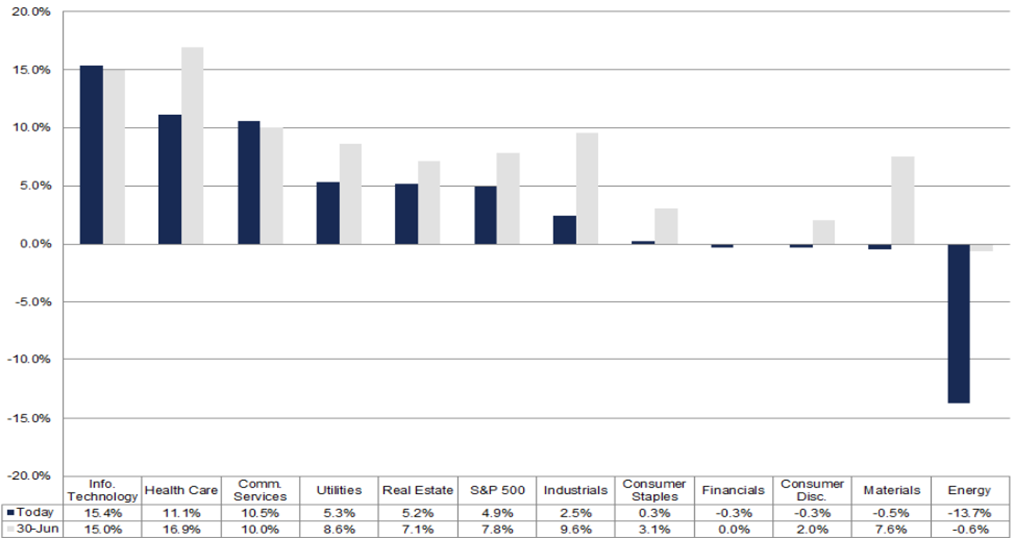

With the third quarter wrapping up, projected earnings for the S&P 500 are still lower than at the beginning of the quarter. Despite this dip, the index is on track to post year-over-year earnings growth for the fifth consecutive quarter. Looking ahead, analysts are optimistic about double-digit earnings growth starting again in Q4 2024. As of mid-September, the estimated earnings growth for the S&P 500 in Q3 2024 stands at 4.9%, down from the 7.8% estimate back at the end of June.

Nine sectors have faced downward revisions in earnings estimates, with Energy, Industrials, Materials, and Health leading the pack. On the flip side, Communication Services and Information Technology have seen upward revisions, reflecting brighter expectations.

3Q24 S&P 500 Earnings Growth YoY by Sector

Source: Factset (As of September 13)

The bull case: Nvidia’s AI power play fuels Tech sector’s Q3 growth

The Information Technology sector is set to lead the pack in Q3, with a projected year-over-year earnings growth of 15.4%, the highest of all 11 sectors. Breaking it down by industry, five out of six are expected to post solid growth:

The only outlier? Communications Equipment, with a predicted 16% drop in earnings.

Nvidia (NVDA) is a key player in this surge, expected to post EPS of $0.74 vs. $0.40 last year, driving a huge chunk of the sector's growth. Excluding Nvidia, the sector’s growth rate would plummet from 15.4% to 8.0%.

Nvidia crushed its Q2 earnings in late August, blowing past expectations with revenue up 122% year-over-year, and adjusted EPS more than doubling. This signals that the AI boom is far from cooling down, with Nvidia far ahead of competitors thanks to its pricing power and financial dominance — as reflected in the charts below.

Nvidia vs Key Chipmaker Comps - Revenue Growth and EBIT Margin

Source: Seeking Alpha

The bear case: Energy sector slashed amid falling oil

On the flip side, the Energy sector has seen the steepest drop in estimated earnings growth since the start of the quarter. The sector's expected year-over-year earnings decline has grown from -0.6% on June 30 to a much sharper -13.7% as of September 13th. A major factor behind this decline is the roughly 15% drop in oil prices since the end of June.

Brent Crude Oil Price Index ($/Bbl)

Source: Trading Economics

In total, 77% of companies in the Energy sector (17 out of 22) have had their mean EPS estimates downgraded. Among the hardest hit, six companies saw their estimates drop by more than 15%, with Marathon Petroleum (MPC) down to $3.00 from $5.45, Valero Energy (VLO) down to $2.84 from $4.45, and Phillips 66 (PSX) down to $2.47 from $3.59. Exxon Mobil (XOM) and Chevron (CVX) also faced downward revisions, dropping from $2.47 to $2.10, and $3.42 to $2.89 respectively.

Reply